The SEC has acknowledged that the COVID-19 public health crisis is presenting challenges for some entities and individuals applying for EDGAR codes. In particular, they are having difficulty meeting the notary requirement in the Form ID access application process and other EDGAR access processes that require notarization. The SEC has stated that it is “considering options to address this matter”. In the meantime they encourage anyone experiencing difficulties in meeting the notarization requirement in Form ID or related access processes due to the COVID-19 crisis to contact Filer Support at 202-551-8900 option 3.

Howard Berkenblit

Recent Posts

In light of coronavirus concerns, the SEC issued some guidance and relief from filing conditions for companies thinking of switching to virtual shareholder meetings or delaying their meetings after their initial proxy materials have been sent, as well as encouraging companies to allow proponents of shareholder proposals to present their proposals remotely rather than in person:

0 Comments Click here to read/write comments

Topics: SEC Filings, shareholder, coronavirus, COVID-19, virtual shareholder meetings

The SEC’s Division of Corporation Finance published additional guidance regarding disclosure obligations that companies should consider with respect to intellectual property and technology risks that may occur when they engage in international operations. While the guidance does not contain any new rules or interpretations, it is a good reminder for companies to review their IP and cybersecurity risk factors as they prepare their forthcoming 10-Ks. The guidance includes examples and questions that each company should consider.

Read more here.

0 Comments Click here to read/write comments

The SEC’s EDGAR system will be closed on Tuesday, December 24, 2019, and Wednesday, December 25, 2019, due to the closure of the federal government on those two days. As a result, on December 24 and 25, 2019:

- Filings will not be accepted in EDGAR.

- EDGAR filing websites will not be operational.

- The Filer Support Call Center will not be open.

Any filings required to be made no later than December 24 or December 25, 2019 will be considered timely if filed on or before December 26, 2019, the next business day.

0 Comments Click here to read/write comments

Topics: SEC, EDGAR, SEC Filings

The SEC today proposed amendments to the definition of “accredited investor,” one of the principal tests for who is eligible to participate in exempt private placements of securities. According to the SEC, the proposed amendments seek “to update and improve the definition to more effectively identify institutional and individual investors that have the knowledge and expertise to participate in our private capital markets.”

Besides the existing qualifications based on income or net worth, the amendments would add additional means for individuals to qualify as accredited investors by adding new categories based on their professional knowledge, experience, or certifications. In addition, the amendments would expand the list of entities that may qualify as accredited investors by, among other things, including a “catch-all” category for any entity owning in excess of $5 million in investments. The proposed amendments would also expand the list of eligible entities under the definition of “qualified institutional buyer” under Rule 144A under the Securities Act.

More specifically, the proposed amendments would make the following changes to the accredited investor definition:

- add new categories that would permit natural persons to qualify based on certain professional certifications and designations, such as a Series 7, 65 or 82 license, or other credentials issued by an accredited educational institution;

- with respect to investments in a private fund, add a new category based on the person’s status as a “knowledgeable employee” of the fund;

- add limited liability companies that meet certain conditions, registered investment advisers and rural business investment companies (RBICs) to the current list of entities that may qualify as accredited investors;

- add a new category for any entity, including Indian tribes, owning “investments,” as defined in Rule 2a51-1(b) under the Investment Company Act, in excess of $5 million and that was not formed for the specific purpose of investing in the securities offered;

- add “family offices” with at least $5 million in assets under management and their “family clients,” as each term is defined under the Investment Advisers Act; and

- add the term “spousal equivalent” to the accredited investor definition, so that spousal equivalents may pool their finances for the purpose of qualifying as accredited investors.

The proposed amendments to the qualified institutional buyer definition in Rule 144A would add limited liability companies and RBICs to the types of entities that are eligible for qualified institutional buyer status if they meet the $100 million in securities owned and investment threshold in the definition. The proposed amendments would also add a “catch-all” category that would permit institutional accredited investors under Rule 501(a), of an entity type not already included in the qualified institutional buyer definition, to qualify as qualified institutional buyers when they satisfy the $100 million threshold.

The proposed amendments will be subject to a 60-day public comment period, after which the SEC will decide whether to proceed to final rulemaking.

0 Comments Click here to read/write comments

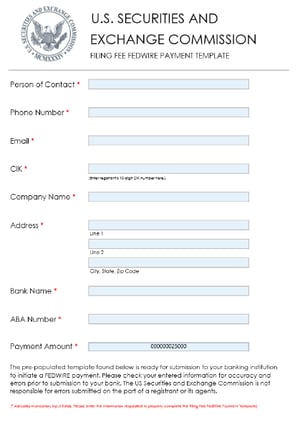

If a wire transfer of SEC filing fees does not contain the required information in the proper format, the acceptance of your filing could be delayed. It is critical that you provide to your sending bank or wire transfer service all required information—including the payor’s SEC-assigned CIK (Central Index Key) and the U.S. Treasury account number designated for SEC filers. To receive proper credit, this information must be inserted in the proper fields as well as in the proper format.

To help facilitate this process, we encourage you to use our pre-populated Filing Fee FEDWIRE Payment Template.

For more information on SEC filing fee payment options, please refer to the Payment Options webpage and select the “Filing Fee Registrants” payee type.

0 Comments Click here to read/write comments

Topics: SEC Filings

Yesterday, the SEC proposed amendments (https://www.sec.gov/rules/proposed/2019/33-10720.pdf) that would modernize filing fee disclosure and payment methods for most SEC forms that require fees to be paid. The amended rules, if approved, would require each fee table and accompanying disclosure to include all required information for fee calculation (not just certain aspects, as is the case under the current rules) in a structured format using inline XBRL. This would purportedly allow the SEC to better automate the fee verification on their end and in theory make the fee process more efficient. The proposed amendments would also add the option for fee payment via Automated Clearing House ("ACH") and eliminate the option for fee payment via paper checks and money orders.

0 Comments Click here to read/write comments

Topics: SEC Filings, Automated Clearing House, ACH

Yesterday the SEC adopted a new rule 163B (Final rule release can be found here) that extends a “test-the-waters” accommodation—currently a tool available to emerging growth companies or “EGCs”—to all issuers.

Under the new rule, all issuers will be allowed to engage in test-the-waters communications with qualified institutional buyers and institutional accredited investors regarding a contemplated registered securities offering prior to, or following, the filing of a registration statement related to such offering. These communications will be exempt from restrictions imposed by Section 5 of the Securities Act on written and oral offers prior to or after filing a registration statement. Under the rule there are no filing or legending requirements; the communications are deemed “offers”; and issuers subject to Regulation FD will need to consider whether any information in a test-the-waters communication would trigger disclosure obligations under Regulation FD or whether an exemption under Regulation FD would apply.

0 Comments Click here to read/write comments

Topics: SEC Filings

As a reminder, effective on Tuesday, October 1st, the SEC’s registration fees will increase to $129.80/million dollars registered, an increase from $121.20/million dollars registered.

It is essential that companies pay the accurate registration fee prior to filing or else their registration statements may be rejected by the SEC.

0 Comments Click here to read/write comments

Topics: SEC Filings

The SEC today requested public comment on ways to simplify, harmonize, and improve the exempt offering framework to expand private investment opportunities while maintaining appropriate investor protections and to promote capital formation.

The concept release seeks input on whether changes should be made to improve the consistency, accessibility and effectiveness of the SEC's exemptions for both companies and investors, including identifying potential overlap or gaps within the framework. It also considers, among other things, whether:

- The limitations on who can invest in certain exempt offerings, or the amount they can invest, provide an appropriate level of investor protection or pose an undue obstacle to capital formation or investor access to investment opportunities

- The SEC should take steps to facilitate a company's ability to transition from one offering to another or to a registered offering

- The SEC should expand companies' ability to raise capital through pooled investment funds

- Retail investors should be allowed greater exposure to growth-stage companies through pooled investment funds such as interval funds and other closed-end funds

- The SEC should revise its exemptions governing the secondary trading of securities initially issued in exempt offerings

Among other things, the SEC poses various questions on topics such as whether there should be any changes to Rule 506 (the release includes a discussion of the "accredited investor" definition), Regulation A, Rule 504, the intrastate offering exemptions and Regulation Crowdfunding and whether there may be gaps in the Commission’s framework that may make it difficult, especially for smaller companies, to rely on an exemption from registration to raise capital at key stages of their business cycle.

The public comment period for the concept release will remain open for 90 days following publication of the release in the Federal Register, following which the SEC may (or may not) propose specific rule changes.

0 Comments Click here to read/write comments

Topics: Regulation A, Securities and Exchange Commission, Rule 504, Rule 506