The Chair of the SEC and the Director of the SEC’s Division of Corporation Finance put out an unusual joint statement emphasizing the importance of disclosures about the potential impacts of COVID-19, particularly in light of upcoming earnings releases and analyst and investor calls. They "urge companies to provide as much information as is practicable regarding their current financial and operating status, as well as their future operational and financial planning." Disclosures should respond to investor interest in: (1) where the company stands today, operationally and financially, (2) how the company’s COVID-19 response, including its efforts to protect the health and well-being of its workforce and its customers, is progressing, and (3) how its operations and financial condition may change as collective efforts to fight COVID-19 progress. Among other things, the statement stresses the need for forward-looking information about the possible consequences to each company (and promises not to second guess companies’ good faith efforts). Notably the statement observes that "Historical information may be relatively less significant." We recommend as each public company considers its upcoming public disclosures to review this statement in detail and try to respond to the expectations and requests that it contains.

As a follow up to the SEC’s previous acknowledgement of processing challenges due to coronavirus issues in preparing Form IDs to obtain EDGAR codes, the SEC has adopted a temporary final rule that provides relief from the notarization requirement from March 26, 2020 through July 1, 2020, subject to certain conditions. Among those conditions are that the filer indicates on its manually signed Form ID that it could not provide the required notarization due to circumstances relating to COVID-19, and that the filer submits a PDF copy of the notarized manually signed document within 90 days of obtaining an EDGAR account.

Topics: EDGAR, SEC Filings, coronavirus, COVID-19

The SEC’s Division of Corporation Finance has issued updated disclosure guidance (https://www.sec.gov/news/press-release/2020-73) providing the SEC staff’s current views regarding disclosure and other securities law obligations that companies should consider with respect to COVID-19 and related business and market disruptions. The guidance again reminds companies that where a company has become aware of a risk related to the Coronavirus that would be material to its investors, it should refrain from engaging in securities transactions with the public and discourage directors and officers (and other corporate insiders who are aware of these matters) from initiating such transactions until investors have been appropriately informed about the risk. To the extent the company or insiders are engaged in transactions, or circumstances otherwise warrant it, the company should consider what disclosures are required in order to inform the public of its financial condition. When companies do disclose material information related to the impacts of the Coronavirus, they are reminded to take the necessary steps to avoid selective disclosures and to disseminate such information broadly. Depending on a company’s particular circumstances, it should consider whether it may need to revisit, refresh, or update previous disclosure to the extent that the information becomes materially inaccurate. Companies providing forward-looking information in an effort to keep investors informed about material developments, including known trends or uncertainties regarding the Coronavirus, can take steps to avail themselves of the normal safe harbor for this information.

Among the areas the guidance discusses for companies to consider are the impact of Coronavirus on:

- financial condition and results of operations, plus future operating results and near-and-long-term financial condition;

- capital and financial resources, including overall liquidity position and outlook (and if a material liquidity deficiency has been identified, what course of action the company has taken or proposes to take to remedy the deficiency);

- cost of or access to capital and funding sources, such as revolving credit facilities or other sources, and access to cash;

- material uncertainty about the ongoing ability to meet the covenants of credit agreements;

- the ability to service debt or other financial obligations, access the debt markets, including commercial paper or other short-term financing arrangements, maturity mismatches between borrowing sources and the assets funded by those sources, changes in terms requested by counterparties, changes in the valuation of collateral, and counterparty or customer risk;

- expected incurrence of any material COVID-19-related contingencies, impairments, increases in allowances for credit losses, restructuring charges, other expenses, or changes in accounting judgments that have had or are reasonably likely to have a material impact on the company’s financial statements;

- the ability to maintain operations, including financial reporting systems, internal control over financial reporting and disclosure controls and procedures, and any changes in controls that occurred during the current period that materially affect or are reasonably likely to materially affect the company’s internal control over financial reporting;

- implementing business continuity plans or required material expenditures to do so;

- demand for products or services;

- supply chain or the methods used to distribute products or services;

- human capital resources and productivity; and

- the ability to operate and achieve business goals due to travel restrictions and border closures.

The guidance also reminds companies of their obligations with respect to the presentation of non-GAAP financial measures, noting that to the extent a company presents a non-GAAP financial measure or performance metric to adjust for or explain the impact of COVID-19, it would be appropriate to highlight why management finds the measure or metric useful and how it helps investors assess the impact of COVID-19 on the company’s financial position and results of operations. The guidance acknowledges that there may be instances where a GAAP financial measure is not available at the time of the earnings release because the measure may be impacted by COVID-19-related adjustments that may require additional information and analysis to complete. In these situations, the guidance states that the Division of Corporation Finance would not object to companies reconciling a non-GAAP financial measure to preliminary GAAP results that either include provisional amount(s) based on a reasonable estimate, or a range of reasonably estimable GAAP results. The provisional amount or range should reflect a reasonable estimate of COVID-19 related charges not yet finalized, such as impairment charges. In addition, the guidance states that if a company presents non-GAAP financial measures that are reconciled to provisional amount(s) or an estimated range of GAAP financial measures, it should limit the measures in its presentation to those non-GAAP financial measures it is using to report financial results to the Board of Directors. If a company presents non-GAAP financial measures that are reconciled to provisional amount(s) or an estimated range of GAAP financial measures, it should explain, to the extent practicable, why the line item(s) or accounting is incomplete, and what additional information or analysis may be needed to complete the accounting.

In addition, as further detailed in our client advisory from last week (https://www.sullivanlaw.com/news-SEC-Provides-Conditional-Regulatory-Relief-for-Public-Companies-Impacted-by-Coronavirus.html), the SEC had offered public companies impacted by coronavirus extensions on their periodic report deadlines for reports due between March 1 and April 30, subject to meeting certain conditions (as described in our advisory). Today, the SEC further extended its relief to filings due between March and July 1.

The SEC has also encouraged companies facing other administrative difficulties in the filing process (e.g., inability to obtain a required signature due to an executive officer being located in a quarantined zone) to contact the staff who will help address these issues on a case-by-case basis in light of their fact-specific nature.

Topics: SEC Filings, coronavirus, COVID-19

The SEC has acknowledged that the COVID-19 public health crisis is presenting challenges for some entities and individuals applying for EDGAR codes. In particular, they are having difficulty meeting the notary requirement in the Form ID access application process and other EDGAR access processes that require notarization. The SEC has stated that it is “considering options to address this matter”. In the meantime they encourage anyone experiencing difficulties in meeting the notarization requirement in Form ID or related access processes due to the COVID-19 crisis to contact Filer Support at 202-551-8900 option 3.

Topics: EDGAR, SEC Filings, coronavirus, COVID-19

In light of coronavirus concerns, the SEC issued some guidance and relief from filing conditions for companies thinking of switching to virtual shareholder meetings or delaying their meetings after their initial proxy materials have been sent, as well as encouraging companies to allow proponents of shareholder proposals to present their proposals remotely rather than in person:

Topics: SEC Filings, shareholder, coronavirus, COVID-19, virtual shareholder meetings

The SEC’s Division of Corporation Finance published additional guidance regarding disclosure obligations that companies should consider with respect to intellectual property and technology risks that may occur when they engage in international operations. While the guidance does not contain any new rules or interpretations, it is a good reminder for companies to review their IP and cybersecurity risk factors as they prepare their forthcoming 10-Ks. The guidance includes examples and questions that each company should consider.

Read more here.

The SEC’s EDGAR system will be closed on Tuesday, December 24, 2019, and Wednesday, December 25, 2019, due to the closure of the federal government on those two days. As a result, on December 24 and 25, 2019:

- Filings will not be accepted in EDGAR.

- EDGAR filing websites will not be operational.

- The Filer Support Call Center will not be open.

Any filings required to be made no later than December 24 or December 25, 2019 will be considered timely if filed on or before December 26, 2019, the next business day.

Topics: SEC, EDGAR, SEC Filings

The SEC today proposed amendments to the definition of “accredited investor,” one of the principal tests for who is eligible to participate in exempt private placements of securities. According to the SEC, the proposed amendments seek “to update and improve the definition to more effectively identify institutional and individual investors that have the knowledge and expertise to participate in our private capital markets.”

Besides the existing qualifications based on income or net worth, the amendments would add additional means for individuals to qualify as accredited investors by adding new categories based on their professional knowledge, experience, or certifications. In addition, the amendments would expand the list of entities that may qualify as accredited investors by, among other things, including a “catch-all” category for any entity owning in excess of $5 million in investments. The proposed amendments would also expand the list of eligible entities under the definition of “qualified institutional buyer” under Rule 144A under the Securities Act.

More specifically, the proposed amendments would make the following changes to the accredited investor definition:

- add new categories that would permit natural persons to qualify based on certain professional certifications and designations, such as a Series 7, 65 or 82 license, or other credentials issued by an accredited educational institution;

- with respect to investments in a private fund, add a new category based on the person’s status as a “knowledgeable employee” of the fund;

- add limited liability companies that meet certain conditions, registered investment advisers and rural business investment companies (RBICs) to the current list of entities that may qualify as accredited investors;

- add a new category for any entity, including Indian tribes, owning “investments,” as defined in Rule 2a51-1(b) under the Investment Company Act, in excess of $5 million and that was not formed for the specific purpose of investing in the securities offered;

- add “family offices” with at least $5 million in assets under management and their “family clients,” as each term is defined under the Investment Advisers Act; and

- add the term “spousal equivalent” to the accredited investor definition, so that spousal equivalents may pool their finances for the purpose of qualifying as accredited investors.

The proposed amendments to the qualified institutional buyer definition in Rule 144A would add limited liability companies and RBICs to the types of entities that are eligible for qualified institutional buyer status if they meet the $100 million in securities owned and investment threshold in the definition. The proposed amendments would also add a “catch-all” category that would permit institutional accredited investors under Rule 501(a), of an entity type not already included in the qualified institutional buyer definition, to qualify as qualified institutional buyers when they satisfy the $100 million threshold.

The proposed amendments will be subject to a 60-day public comment period, after which the SEC will decide whether to proceed to final rulemaking.

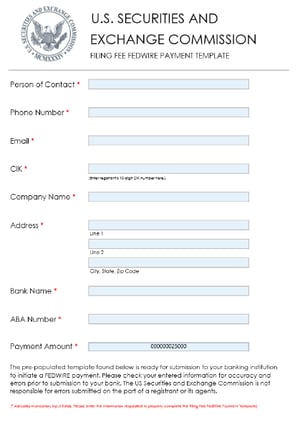

If a wire transfer of SEC filing fees does not contain the required information in the proper format, the acceptance of your filing could be delayed. It is critical that you provide to your sending bank or wire transfer service all required information—including the payor’s SEC-assigned CIK (Central Index Key) and the U.S. Treasury account number designated for SEC filers. To receive proper credit, this information must be inserted in the proper fields as well as in the proper format.

To help facilitate this process, we encourage you to use our pre-populated Filing Fee FEDWIRE Payment Template.

For more information on SEC filing fee payment options, please refer to the Payment Options webpage and select the “Filing Fee Registrants” payee type.

Topics: SEC Filings

Yesterday, the SEC proposed amendments (https://www.sec.gov/rules/proposed/2019/33-10720.pdf) that would modernize filing fee disclosure and payment methods for most SEC forms that require fees to be paid. The amended rules, if approved, would require each fee table and accompanying disclosure to include all required information for fee calculation (not just certain aspects, as is the case under the current rules) in a structured format using inline XBRL. This would purportedly allow the SEC to better automate the fee verification on their end and in theory make the fee process more efficient. The proposed amendments would also add the option for fee payment via Automated Clearing House ("ACH") and eliminate the option for fee payment via paper checks and money orders.

Topics: SEC Filings, Automated Clearing House, ACH